NCUA Governance & Account Insurance

What is NCUA?

NCUA -- short for the National Credit Union Administration -- is an independent federal government agency that charters and supervises federal credit unions and insures accounts in federal and most state-chartered credit unions across the country through the National Credit Union Share Insurance Fund (NCUSIF), a federal fund backed by the full faith and credit of the United States government.

What is the purpose of NCUSIF?

The NCUSIF protects members’ accounts in federally insured credit unions, in the unlikely event of a credit union failure. The NCUSIF covers the balance of each member’s account, dollar-for-dollar up to the insurance limit, including principal and posted dividends through the date of the failure.

What is the NCUSIF insurance amount?

Properly established member accounts in federally insured credit unions are insured up to the Standard Maximum Share Insurance Amount (SMSIA). The basic insurance amount is $250,000 per individual account holder, per federally insured credit union. This includes principal and posted dividends up to a total of $250,000. Joint account holders are insured up to $250,000 per joint account holder, per federally insured credit union. For example, an account with two joint account holders is insured for $500,000 separately from the holders’ individual accounts. This includes principal and posted dividends. IRA and KEOGH accounts are insured, separate from other accounts, up to $250,000 per institution, including principal and posted dividends.

What does NCUSIF insure?

The NCUSIF insures all types of deposits received by a credit union in its usual course of business. For example, savings accounts, share draft (checking) accounts, money market accounts, and share certificates (certificates of deposit “CDs”) are all insured by the NCUSIF.

What is not insured by NCUSIF?

The NCUSIF does not insure the money individuals invest in stocks, bonds, municipal bonds, or other securities such as mutual funds (including money market mutual funds, and mutual funds that invest in stocks, bonds and other securities); annuities (which are contracts underwritten by insurance companies that guarantee income in exchange for a lump sum or periodic payment); or insurance products such as automobile and life insurance, even if these products were purchased at a federally insured credit union or through an affiliated broker/dealer/insurance agent that is offering these products on behalf of a federally insured credit union.

The NCUSIF does not insure U.S. Treasury bills, bonds, or notes, but these are backed by the full faith and credit of the U.S. Government.

Also, the NCUSIF doesn't cover valuables in safe deposit boxes. These contents; however, may be covered by a box holder's personal homeowner's insurance.

What types of financial institutions are insured by NCUA’s NCUSIF?

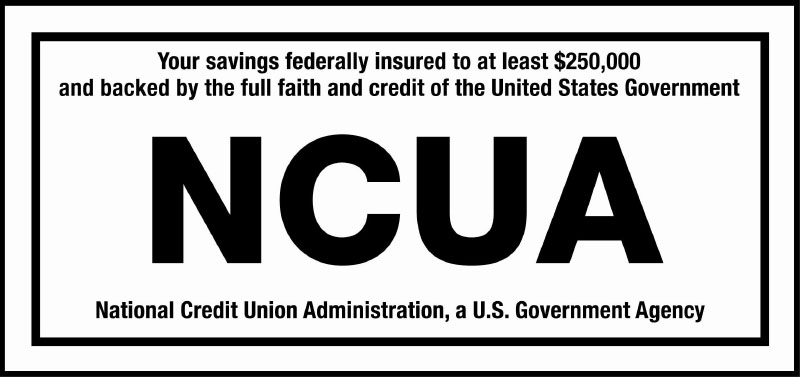

NCUA insures accounts in all federally chartered credit unions and most state-chartered credit unions. All NCUA insured institutions must display this official sign at each teller window or teller station.

Can insurance coverage be increased by depositing funds with different federally insured credit unions?

Member accounts at each NCUA insured credit union are insured separately from any accounts held at another federally insured credit union. If an insured credit union has branch offices, the main office and all branch offices are considered one credit union for insurance purposes. A member cannot increase insurance coverage by placing deposits at different branches of the same federally insured credit union. Similarly, member accounts held with the Internet division of a federally insured credit union are considered the same as funds deposited with the "brick and mortar" part of the credit union, even if the Internet division uses a different name.

Can insurance coverage be increased by dividing my deposits into several different accounts at the same federally insured credit union?

Share insurance coverage can be increased only if accounts are held in different categories of ownership. These categories include the four most common consumer ownership categories: single owner accounts, retirement accounts, joint accounts, and revocable trust accounts; and less common ownership categories such as irrevocable trust accounts, employee benefit plan accounts, corporation, partnership and unincorporated association accounts, and public unit or government depositor accounts.

A credit union member cannot increase federal insurance by dividing funds owned in the same ownership category among different accounts. The type of member account - whether savings accounts, share draft (checking) account, or share certificate (certificate of deposit “CD”) - has no bearing on the amount of insurance coverage.

Can insurance coverage be increased by using a different co-owner's Social Security number on each account or changing the way the owners' names are listed on the accounts?

Using different Social Security numbers, rearranging the order of names listed on accounts or substituting "and" for "or" in joint account titles does not affect the amount of insurance coverage available to account owners.

How does NCUA determine ownership of funds?

The NCUA relies on "account records" of the federally insured credit union to determine how funds are insured. The NCUA may request supplemental documentation to identify relationships between owners and beneficiaries. These documents may be used by the NCUA to confirm that the funds are actually owned in the manner indicated in the credit union’s account records and to determine the amount of insurance coverage.

What are "account records?"

The "account records" of a federally insured credit union are, for example, account ledgers, signature cards, share certificates, passbooks, and certain computer records.

What is share insurance coverage after a member dies?

The NCUA will insure a deceased member's accounts as if he or she were still alive for six months after a member owner’s death. During this "grace period," the insurance coverage of the member owner's accounts will not change unless the accounts are restructured by those authorized to do so. The NCUA applies the grace period only if its application would increase, rather than decrease, share insurance coverage.

For example: A and B own a qualifying joint account of $500,000 for which they each have a right of survivorship. B also has a single (or individual) account of $250,000 at the same NCUA-insured institution. If A dies, for six months after A's death the NCUA will still insure the A and B account as a joint account, even though B, as A's survivor, has inherited A's ownership interest in the account. After the grace period, B's increased ownership interest in the joint account would be added to his or her single account and insured to a limit of $250,000.

Please note this grace period does not extend to beneficiaries listed on revocable trust accounts (also known as “payable on death” or “in trust for” accounts).

What happens when federally insured credit unions merge?

If a member has accounts in credit union A and credit union B, and credit union A merges into credit union B, accounts of credit union A continue to be insured separately from the deposits of credit union B for at least six months after the date of the merger. Share certificates from credit union A, the merged credit union, are separately insured until the earliest maturity date after the end of the six month grace period

What happens if a federally insured credit union is liquidated?

The NCUA would either transfer the insured member's account to another NCUA insured credit union or give the federally insured member depositor a check equal to their insured account balance. This includes the principal and posted dividends through the date of the credit union’s liquidation, up to the insurance limit.

If a credit union is liquidated, what is the timeframe for payout of the funds that are insured if the credit union cannot be acquired by another credit union?

Federal law requires the NCUA to make payments of insured accounts "as soon as possible" upon the failure of a federally insured credit union. While every credit union failure is unique, there are standard policies and procedures that the NCUA follows in making share insurance payments. Historically, insured funds are available to members within just a few days after the closure of an insured credit union.

What happens to members with uninsured shares?

Members who have uninsured shares may recover a portion of their uninsured shares, but there is no guarantee that they will recover any more than the insured amount. The amount of uninsured shares they may receive, if any, is based on the recovery of the failed credit union’s assets. Depending on the quality and value of these assets, it may take several years to conclude recovery on all the assets. As recoveries are made, uninsured account holders may receive periodic payments on their uninsured shares claim.

What happens to my direct deposits if a federally insured credit union is liquidated?

If a liquidated credit union is acquired by another federally insured credit union, all direct deposits, including Social Security checks or paychecks delivered electronically, will be automatically deposited into your account at the assuming credit union. If the NCUA cannot find an acquirer for the liquidated credit union, the NCUA will advise members to make new arrangements.

What happens to loans a member has at a liquidated federal credit union?

The member remains liable for any payments due on a loan or credit card. The member would continue making payments as they did before the credit union failed until they are instructed to do otherwise in writing by the acquiring credit union or the NCUA.

If a member's credit union is liquidated and the member has both a loan and shares at the credit union, the NCUA may deduct the loan balance from the share balance.

Source:NCUA

NOTICE OF EXPIRING TEMPORARY NCUA INSURANCE

Insurance on Noninterest-Bearing Transaction Accounts

Section 343 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2012 provided temporary unlimited share/deposit insurance coverage on all noninterest-bearing transaction accounts in federally insured credit unions and banks. Generally, this refers to non-interest bearing share draft/checking accounts with funds in excess of $250,000. As of September 30, 2012, approximately 12.5 percent of credit unions held noninterest-bearing share accounts totaling $2.8 billion. The unlimited share/deposit insurance coverage on noninterest-bearing accounts will expire on December 31, 2012.

Insurance coverage on noninterest-bearing transaction accounts will return to the permanent level of up to $250,000 beginning January 1, 2013. In other words, noninterest-bearing transaction accounts will be subject to the same insurance coverage levels as all other share accounts in a credit union.

For more information visit www.ncua.gov

How your accounts are Federally insured

Your savings are federally insured to at least $250,000 and backed by the full faith and credit of the United States Government. Learn more.

For more information:

Call Toll-free 1-800-755-1030, option 1

Read more about NCUA Share Insurance at MyCreditUnion.gov

Calculate share insurance coverage Use NCUA’s Share Insurance Estimator at MyCreditUnion.gov/estimator

Mail:

National Credit Union Administration

Attn: NCUA Consumer

Assistance Center

1775 Duke Street, Alexandria, VA 22314